The Dutch government has determined that, starting from the financial year 2016, micro and small legal entities are required to submit their financial statements using SBR (Standard Business Reporting). What does this obligation mean in practice, and what are the consequences for your organisation?

What is SBR?

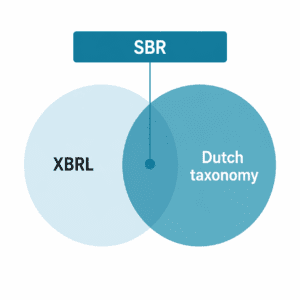

For several years, governments have been working towards a fully digital approach to financial reporting. This initiative is based on XBRL (eXtensible Business Reporting Language). XBRL provides a standardised way to structure, regulate, and exchange both financial and non‑financial data between governments, companies, and other authorities.

To ensure compliance with Dutch legislation for financial reporting, the Dutch taxonomy has been developed. This taxonomy determines which XBRL elements are applicable within the Dutch context. When XBRL is combined with the Dutch taxonomy, it results in SBR, a standardised method for compiling and submitting financial data in a uniform business report.

Figure 1 SBR: XBRL combined with the Dutch taxonomy

How does XBRL work?

XBRL is a standard language for digital business reporting, enabling reporting concepts to be uniquely defined. These reporting concepts are used to represent the content of financial statements. By assigning labels to numbers and text, XBRL can interpret these tags and generate a standardised business report that can be automatically processed by receiving parties.

Which software tools are available?

Various software solutions are available to convert financial and non‑financial data into XBRL format, ranging from Disclosure Management solutions to integrated Excel‑based tools. The most suitable solution for your organisation depends on your own requirements, as well as the expectations of external stakeholders such as the Chamber of Commerce and the Tax Authorities.

One example of a provider offering multiple SBR solutions, including service and conversion tools, is ParsePort. For its conversion solution, ParsePort uses an Excel‑based converter that enables organisations to convert financial statements directly from Excel. The key challenge lies in identifying where each element of the financial statements is located. This is achieved by “tagging” each item with predefined XBRL tags, allowing the converter to correctly interpret the data and generate a standard business report.

Why SBR?

SBR, for example, is used by the following organisations in the Netherlands:

- The Chamber of Commerce

- The Tax Authorities

- The Central Agency for Statistics

- Banks

The Chamber of Commerce

Since December 2015, written financial statements are no longer accepted by the Chamber of Commerce. To support organisations during the transition to digital reporting, the implementation of SBR has been phased. Companies are classified by size based on three criteria, as shown below:

| Criteria | ||||

| Size | Assets | Net-turnover | Number of employees | Effective from |

| Micro | < € 350.000 | < € 700.000 | < 10 employees | Financial year 2016 |

| Small | € 350.000 – € 6M | € 700.000 – € 12M | 10-50 employees | Financial year 2016 |

| Middle | € 6 – € 20M | € 12 – € 40M | 50 – 250 employees | Financial year 2017 |

| Large | > € 20M | > € 40M | > 250 employees | Financial year 2019 |

Figure 2: Different criteria for separating the company size.

The Tax Authority

For the Tax Authorities, receiving financial statements in a standardised format offers clear advantages. It removes ambiguity about required information and reporting formats. As a result, several processes can be handled using SBR, including:

- Request to change or adjust the preliminary assessment of your corporation tax;

- Request a postponement for corporation tax.

The Central Agency for Statistics

In the coming years, the Central Agency for Statistics (CBS) also plans to increasingly use SBR. By leveraging SBR, CBS aims to improve the reliability and consistency of statistical data. To encourage organisations to submit financial data in SBR format, CBS intends to provide valuable insights in return, such as strategic information related to companies’ core business activities.

Banks

Banks have been working towards receiving credit requests in SBR format for several years. As of 2017, banks may charge entrepreneurs a fee of €250 if company information is not submitted in SBR format.

If you would like more information about SBR and how we can support your organisation, please do not hesitate to contact us!