NFRD vs. CSRD

Non-Financial Reporting Directive (NFRD) vs Corporate Sustainability Reporting Directive (CSRD) 22

19 April 2022 – written by Rianne Snijder

In this article, we describe the regulations around Corporate Sustainability Reporting Directive (CSRD). Companies are becoming increasingly aware of their business operations’ social and environmental impact, leading to the introduction of sustainability reporting standards, referred to as Environmental, Social, and Governance reporting (ESG).

ESG reporting helps companies become more transparent in these three main topics, indicative of a company’s sustainability performance and the potential financial risk for investors.

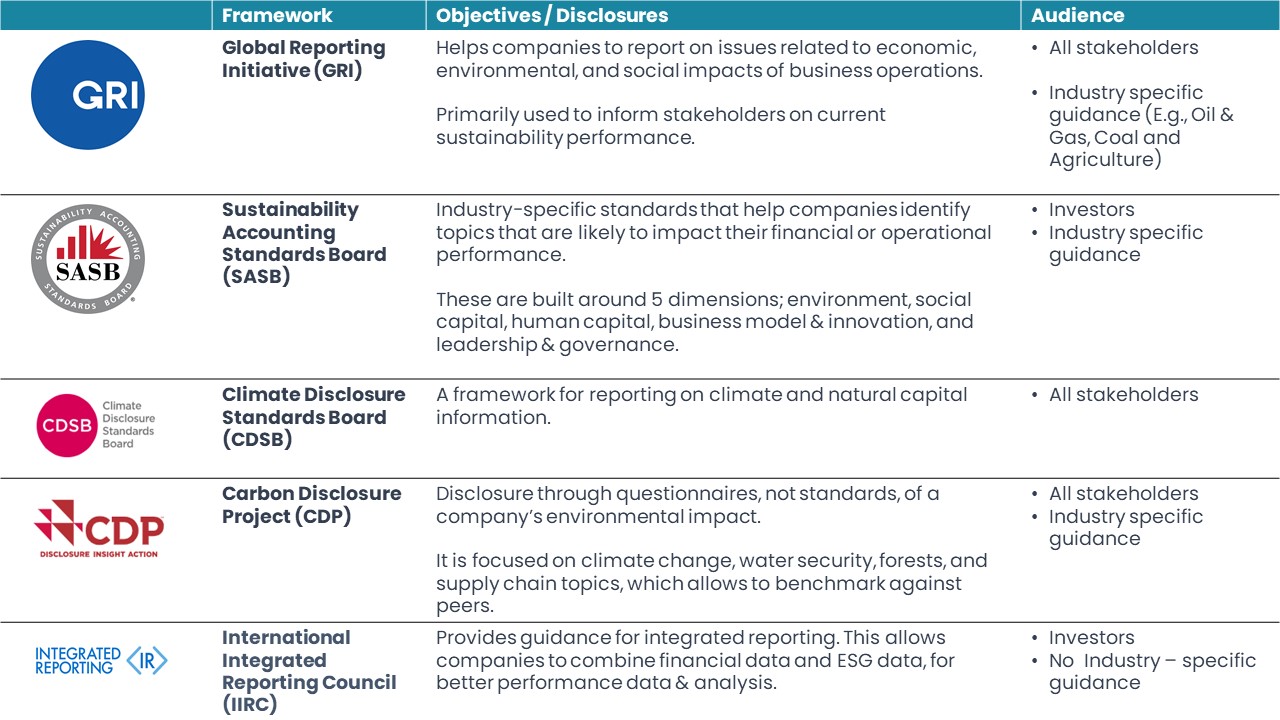

For a group of large, listed companies, ESG reporting is regulated by the Non-Financial Reporting Directive (NFRD). These companies are allowed to choose from different reporting frameworks, such as:

In addition, these companies experience increased data volumes, challenging operational teams to integrate new data reporting standards into their reporting processes rapidly.

Regulation to hold companies accountable for their social and environmental impact is limited under the NFRD, which caused incomparable reports and unreliable data.

As a result, the European Union (EU) announced it is working on a new sustainability directive, named the Corporate Sustainability Reporting Directive (CSRD), and aims to be in effect by 2024 (Fiscal Year 2023).

The CSRD regulation will require more European companies to comply with standards that will improve the reliability and comparability of companies’ social and environmental impact. Based on the existing sustainability reporting standards, the European Financial Reporting Advisory Group (EFRAG) compiles these standards.

In February 2022, the European Council approved the CSRD. It is expected to be approved by the European Parliament in Q2 – Q3 of 2022. After which, it will be sent to the European Commission for ratification.

Cpmview regularly posts updates, blogs, and articles about the developments of the CSRD.

Upcoming topics include:

As we will highlight in our blogs, becoming CSRD compliant will, most likely, become the responsibility of the CFO due to the collection and consolidation of data, monitoring accuracy with internal audits, and external auditing obligations.

With our experience streamlining reporting processes, solving complex data management puzzles, and XHTML formatting, we will guide you to complete your integrated reporting to become CSRD compliant by 2024.

(Updated on 1 June 2022)